How Long Does a Late Payment Affect Your Credit Score? (Expert Guide)

Introduction

A late payment is one of the most common—and damaging—mistakes in personal finance. Whether you miss a credit card bill, a loan EMI, or any other financial obligation, the impact on your credit score can be immediate and long-lasting.

But how long does a late payment actually affect your credit score?

The short answer: up to 7 years.

The real answer is more nuanced—and depends on how late payment was, how often it happens, and how you respond afterward.

In this expert-level guide, we’ll break down everything you need to know about late payments, their impact on your credit score, timelines, recovery strategies, and best practices.

📌 1. What is a Late Payment?

A late payment occurs when you fail to pay at least the minimum amount due on a credit account by the due date.

💳 Common Types of Late Payments:

- Credit card bills

- Personal loan EMIs

- Home loan or car loan EMIs

- Buy Now Pay Later (BNPL) dues

⏱ Grace Period vs Late Payment

Most lenders offer a grace period (2–5 days). If you miss this window, the payment is officially considered late.

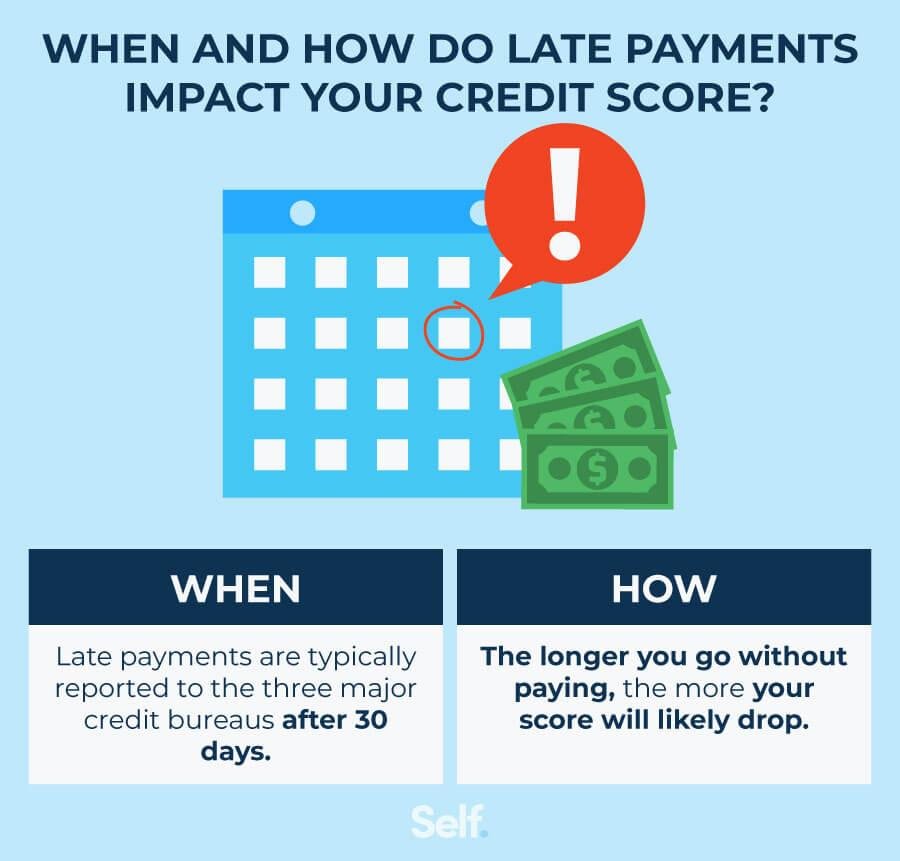

📌 2. When Does a Late Payment Affect Your Credit Score?

Not all late payments impact your credit score immediately. The effect depends on how many days late the payment is.

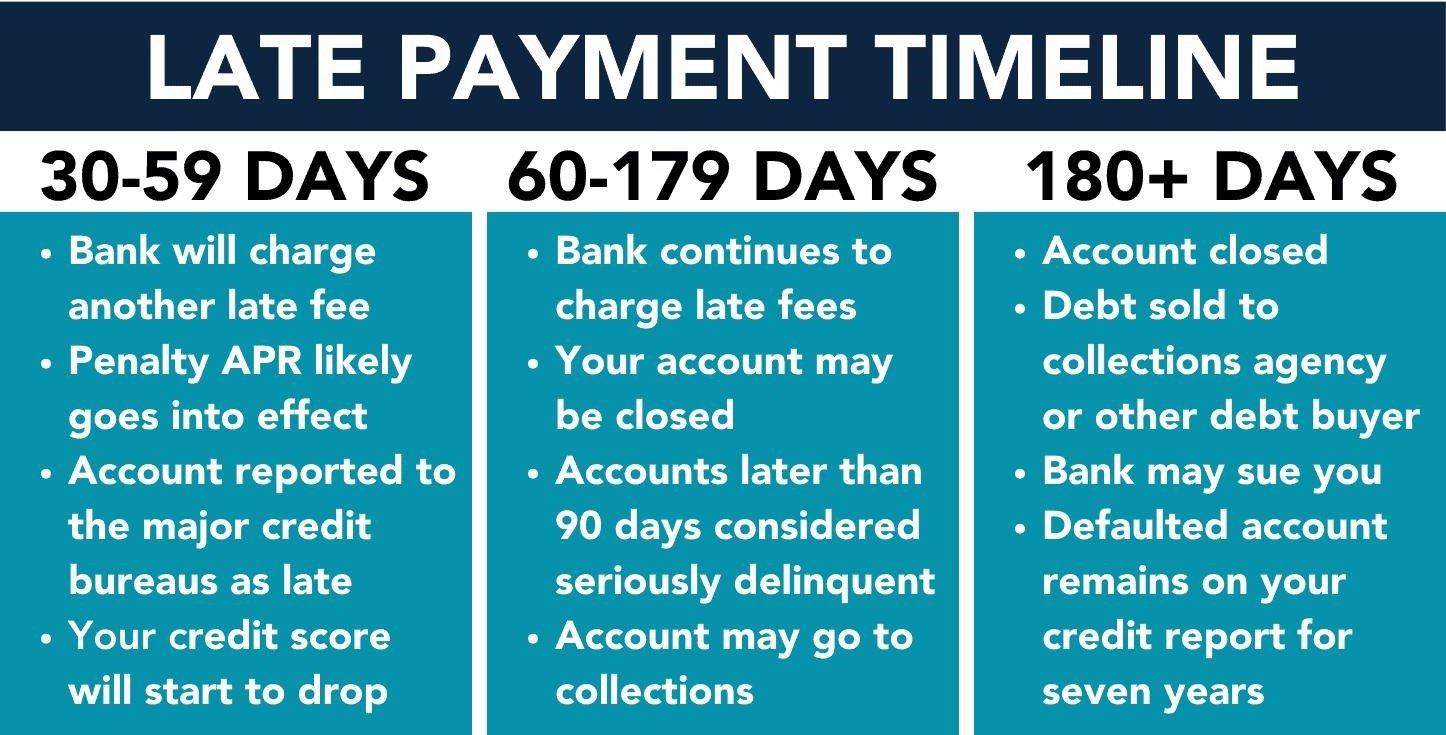

📊 Timeline of Impact:

| Days Late | Impact on Credit Score |

|---|---|

| 1–29 days | Usually no report to credit bureau |

| 30 days late | Reported → Score drops |

| 60 days late | Bigger negative impact |

| 90 days late | Severe damage |

| 120+ days | Account may go into default |

👉 Important: Once a payment crosses 30 days late, it is reported to credit bureaus like CIBIL, Experian, or Equifax.

📌 3. How Long Does a Late Payment Stay on Your Credit Report?

⏳ Standard Rule:

A late payment can stay on your credit report for up to 7 years from the date of delinquency.

📉 But Here’s the Key Insight:

- The impact is strongest in the first 6–24 months

- Over time, the negative effect gradually reduces

- New positive behavior can offset the damage

📌 Example:

If you missed a payment in January 2026, it may remain visible until January 2033, but its impact will reduce significantly after 1–2 years if you maintain good payment behavior.

📌 4. How Much Does a Late Payment Affect Your Credit Score?

The exact drop depends on your existing credit profile.

📊 Estimated Impact:

| Credit Profile | Score Drop |

|---|---|

| Excellent (750+) | 80–100 points |

| Good (700–750) | 60–80 points |

| Fair (650–700) | 40–60 points |

| Poor (<650) | Smaller drop but still harmful |

👉 Irony: The better your score, the more it can drop.

📌 5. Factors That Influence the Impact Duration

Not all late payments are equal. Several factors determine how long and how severely your score is affected.

🔍 Key Factors:

1. Severity of Delay

- 30 days late → Mild damage

- 90+ days late → Severe damage

2. Frequency

- One missed payment → Recoverable

- Multiple late payments → Long-term damage

3. Credit History Length

- Long history → Less impact

- Short history → More impact

4. Overall Credit Behavior

- Consistent payments after → Faster recovery

- Continued delays → Score keeps falling

📌 6. Can You Recover from a Late Payment?

Yes, absolutely. A late payment is not permanent damage.

✅ Recovery Timeline:

- 0–3 months: Major impact

- 3–12 months: Gradual improvement

- 12–24 months: Significant recovery

- 24+ months: Minimal impact (if no further issues)

🚀 How to Recover Faster:

✔ Pay All Future Bills on Time

Payment history = 35% of your score

✔ Reduce Credit Utilization

Keep usage below 30%

✔ Avoid New Debt

Too many loans worsen your profile

✔ Maintain Old Accounts

Length of credit history matters

📌 7. Real-Life Scenario Example

📌 Case Study:

Rahul (Score: 780) misses a credit card payment by 45 days.

- Score drops to ~700

- After 6 months of on-time payments → improves to ~730

- After 1 year → ~750

- After 2 years → ~770

👉 Lesson: Recovery is possible with discipline.

📌 8. Difference Between Late Payment & Default

| Factor | Late Payment | Default |

|---|---|---|

| Duration | 30–90 days | 120+ days |

| Impact | Moderate to High | Severe |

| Recovery | Possible in 1–2 years | Takes longer |

| Legal Action | No | Possible |

📌 9. How to Avoid Late Payments

🛡 Smart Strategies:

- ✔ Set Auto-Debit / AutoPay

- ✔ Use payment reminders

- ✔ Maintain emergency funds

- ✔ Track due dates in calendar

- ✔ Pay at least minimum due

📌 10. Advanced Expert Tips

💡 1. Goodwill Adjustment

You can request your lender to remove a late payment (rare but possible).

💡 2. Dispute Errors

If wrongly reported, file a dispute with the credit bureau.

💡 3. Partial Payment Strategy

Even partial payment can sometimes reduce penalties.

💡 4. Credit Builder Loans

Use small loans to rebuild credit.

📌 11. Key Takeaways

✔ Late payments affect your credit score for up to 7 years

✔ Maximum damage occurs in the first 1–2 years

✔ Even a single 30-day delay can drop your score significantly

✔ Consistent on-time payments can help you recover

✔ Prevention is always better than repair