In India, rising medical inflation—often 10–15% annually—means a single hospitalization can wipe out years of savings. For families, the stakes are even higher: parents, children, and aging grandparents each have unique health risks. A well-chosen health insurance policy isn’t just a tax-saving tool (Section 80D); it’s a financial shield. Use this 1Health Insurance Checklist for Indian Families to make an informed, confident purchase.

Health insurance is no longer optional for Indian families—it’s a financial safety net that protects your savings during medical emergencies. With rising healthcare costs in cities like Gurgaon, Delhi, and Mumbai, even a single hospitalization can cost lakhs. Choosing the right policy requires careful evaluation, not impulse buying.

This Health Insurance Checklist for Indian Families will help you make a smart, informed decision before buying health insurance for your family.

1. Understand Your Family’s Needs

Before selecting a policy, analyze:

- Number of family members

- Age of each member

- Medical history (diabetes, BP, heart issues)

- Lifestyle (sedentary, active, smoker)

- City of residence (metro vs tier-2)

👉 Example: A 38-year-old working professional with parents needs higher coverage compared to a young couple.

Pro Tip: If your parents are above 60, consider separate senior citizen plans.

2. Choose the Right Type of Plan

There are mainly 3 types:

✔ Individual Plan

- Separate coverage for each member

- Higher premium

✔ Family Floater Plan (Best for most families)

- One sum insured shared by all members

- Cost-effective

✔ Senior Citizen Plan

- Designed for parents above 60

- Covers age-related diseases

👉 Checklist Tip:

For a family of 3–4, a floater plan of ₹10–20 lakh is recommended in metro cities.

3. Check Sum Insured Carefully

Medical inflation in India is rising at 10–15% annually.

Recommended Coverage:

- Small cities: ₹5–10 lakh

- Metro cities: ₹10–25 lakh

- With parents: ₹25 lakh+ (or super top-up)

👉 Always choose higher coverage + top-up plan instead of a low base policy.

4. Network Hospitals (Cashless Facility)

Check whether your preferred hospitals are in the insurer’s network.

Why it matters:

- Cashless treatment = No upfront payment

- Faster claim processing

👉 Always verify nearby hospitals in Gurgaon/Delhi NCR before buying.

5. Waiting Period Clauses

Every policy has waiting periods:

- Initial waiting period: 30 days

- Pre-existing diseases: 2–4 years

- Specific diseases: 1–2 years

👉 If you already have diabetes or BP, choose plans with shorter waiting periods.

6. Check Room Rent Limits

Many policies limit room rent (e.g., ₹5,000/day).

Why important:

- Choosing a higher room leads to proportionate deductions

- Final claim amount reduces

👉 Prefer policies with:

- No room rent limit

- Or “single private room” coverage

7. Co-payment Clause

Co-pay means you pay a portion of the bill.

Example:

- 20% co-pay → You pay ₹20,000 on ₹1 lakh bill

👉 Avoid high co-pay unless premium is too expensive.

8. Pre & Post Hospitalization Coverage

Check coverage for:

- Pre-hospitalization (30–60 days)

- Post-hospitalization (60–180 days)

👉 This includes tests, medicines, follow-ups—often expensive but ignored.

9. Daycare Procedures Coverage

Modern treatments don’t require 24-hour hospitalization.

Examples:

- Cataract surgery

- Chemotherapy

- Dialysis

👉 Ensure your plan covers 100+ daycare procedures.

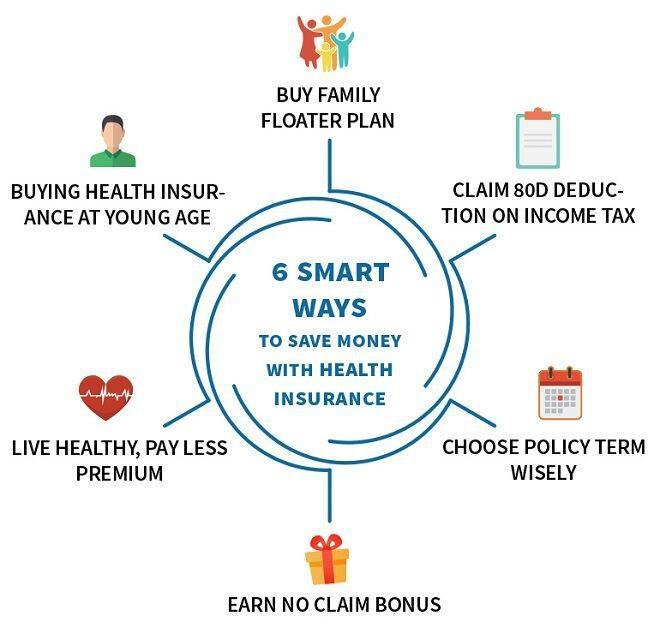

10. No Claim Bonus (NCB)

If no claim is made:

- Sum insured increases (10–50% yearly)

- Or premium discount

👉 Choose policies with cumulative bonus up to 100–200%.

11. Restore Benefit (Refill Coverage)

If your sum insured gets exhausted:

- Insurance refills automatically

👉 Very useful for family floater plans.

12. Check Exclusions Carefully

Common exclusions:

- Cosmetic surgery

- Dental treatments

- Self-inflicted injuries

- Non-allopathic treatments (in some plans)

👉 Always read the fine print before buying.

13. Maternity & Newborn Coverage

If planning a child:

- Check maternity coverage

- Waiting period: 2–4 years

- Newborn cover benefits

👉 Buy early to complete waiting period before pregnancy.

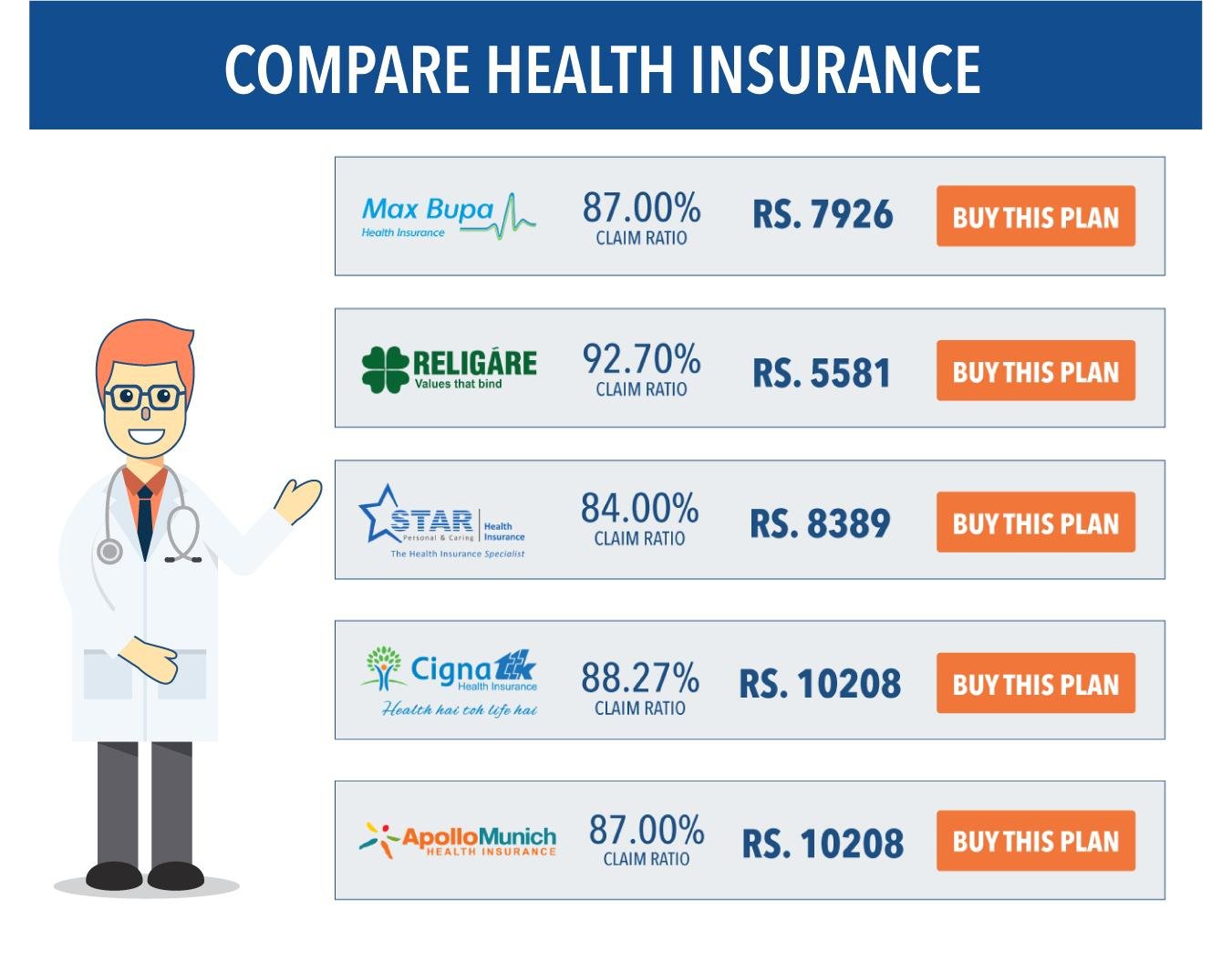

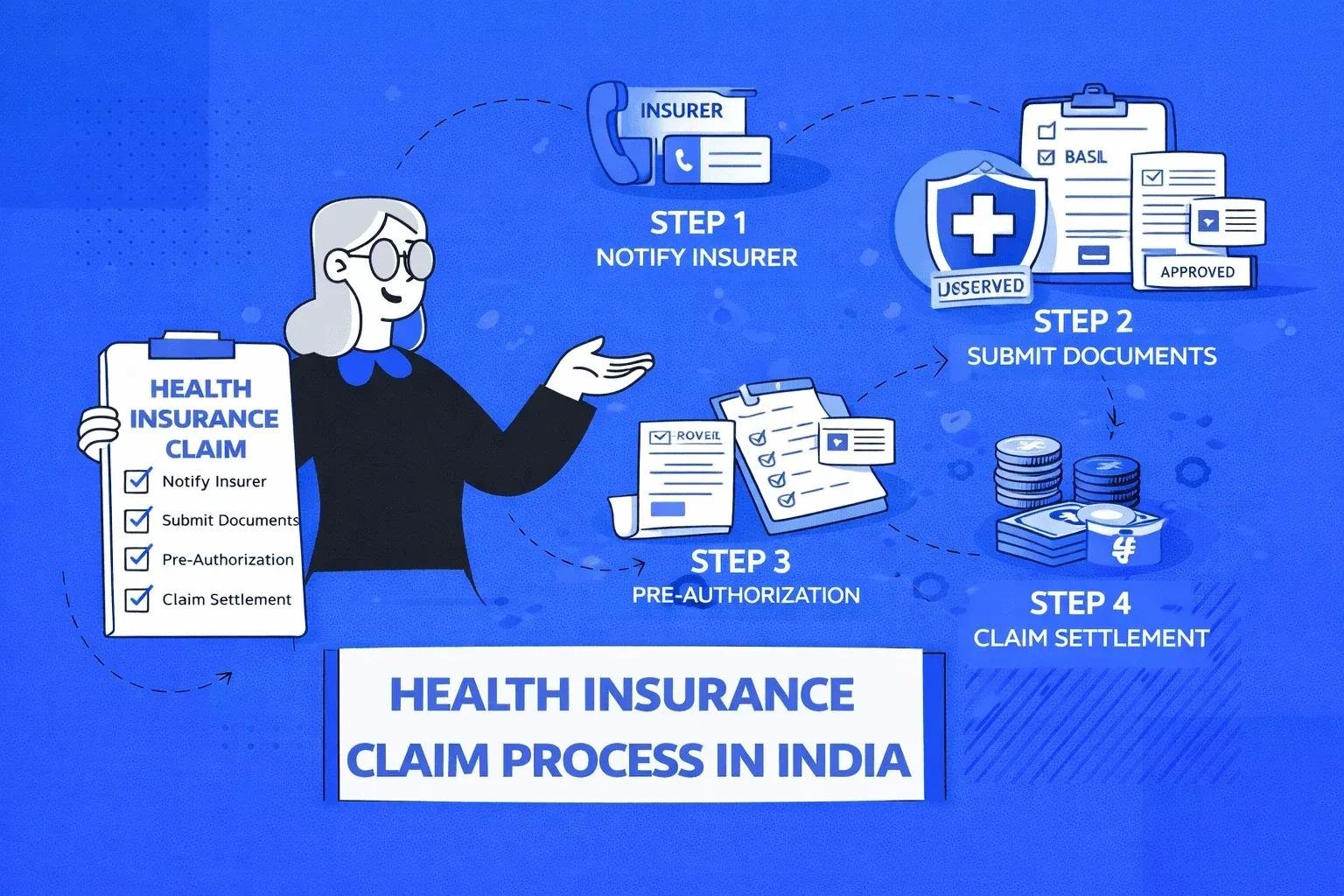

14. Claim Settlement Ratio

Choose insurers with:

- High claim settlement ratio (above 90%)

- Good customer reviews

- Fast processing

👉 Reliability matters more than cheap premium.

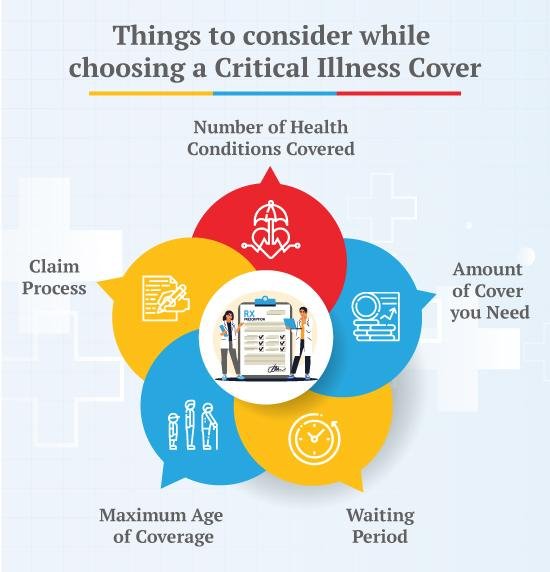

15. Add-ons (Riders)

Useful add-ons:

- Critical illness cover

- Personal accident cover

- OPD cover

- Super top-up

👉 Customize policy based on your needs.

16. Premium vs Coverage Balance

Don’t just go for cheapest policy.

👉 Focus on:

- Coverage adequacy

- Benefits

- Long-term usability

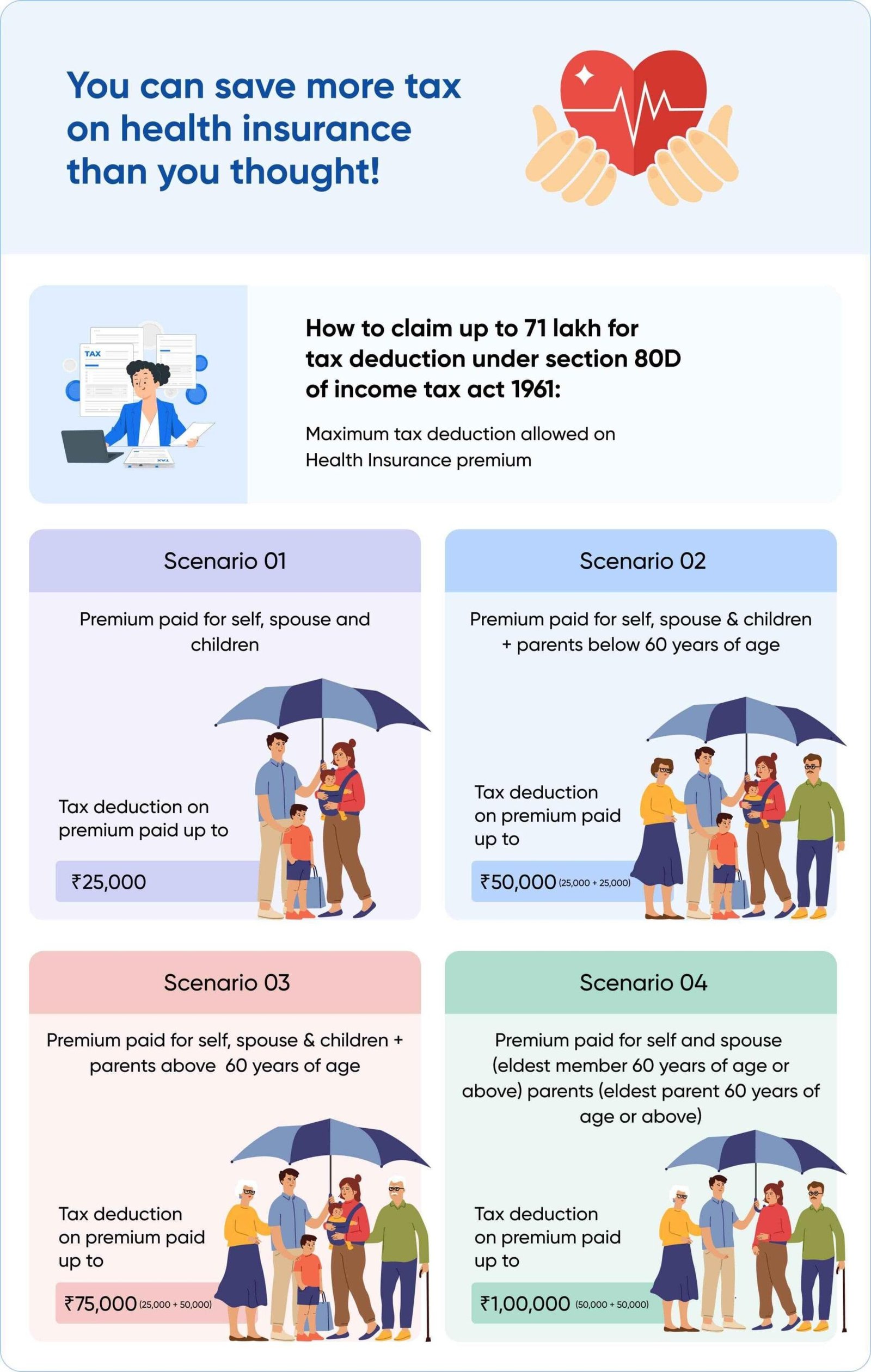

17. Tax Benefits (Section 80D)

You can claim tax deduction:

- ₹25,000 (self + family)

- ₹50,000 (parents, senior citizens)

👉 Health insurance = protection + tax saving.

Final Checklist Summary ✅

Before buying, confirm:

✔ Right plan type (floater/individual)

✔ Adequate sum insured (₹10–25 lakh)

✔ Network hospitals nearby

✔ No/low room rent limits

✔ Minimal co-payment

✔ Short waiting period

✔ Daycare + pre/post hospitalization covered

✔ High claim settlement ratio

✔ Add-ons as needed

✔ Affordable long-term premium

Health insurance is not just a policy—it’s a financial shield for your family’s future. A well-chosen plan ensures that medical emergencies don’t destroy your savings or force you into debt.

For Indian families, especially in urban areas like Gurgaon, having at least a ₹15–25 lakh comprehensive cover + top-up plan is becoming essential in 2026.

Take time to compare, read policy documents, and choose wisely.

Because when emergencies strike, the right insurance makes all the difference.