Credit Card vs Personal Loan: Which Is Better in India? (Complete 2026 Guide)

Choosing between a credit card and a personal loan is one of the most common financial decisions in India today. Both options offer quick access to money—but they work very differently.

If you’re confused about which one is better for your needs, this in-depth guide will help you understand features, benefits, costs, risks, and ideal use cases—so you can make a smart financial decision.

📌 Introduction: The Core Difference

At a basic level:

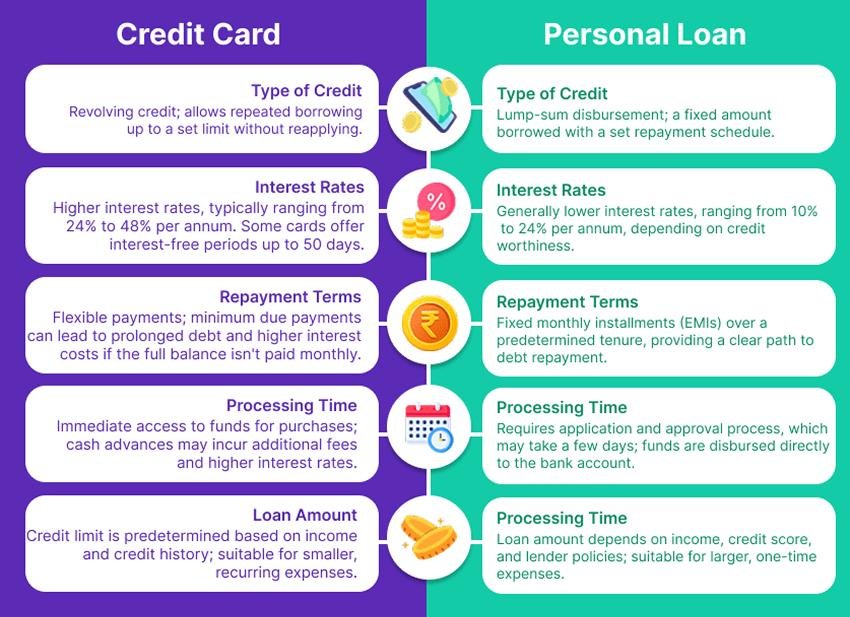

- 💳 Credit Card → A revolving credit line (borrow, repay, reuse)

- 💰 Personal Loan → A fixed lump sum with EMIs

Both are offered by banks like HDFC Bank, ICICI Bank, and State Bank of India.

🧾 What Is a Credit Card?

A credit card allows you to borrow money up to a predefined limit and repay it later—either in full or partially.

🔑 Key Features:

- Interest-free period (up to 45–50 days)

- Minimum payment option

- Rewards, cashback, and offers

- Can be used for shopping, bills, travel

👍 Advantages of Credit Cards

- ✅ Interest-free period (if paid on time)

- ✅ Rewards, cashback, travel points

- ✅ Instant access to funds

- ✅ Builds credit score

👎 Disadvantages of Credit Cards

- ❌ High interest (30%–45% annually) if unpaid

- ❌ Debt trap risk with minimum payments

- ❌ Overspending temptation

💰 What Is a Personal Loan?

A personal loan is a lump sum borrowed from a bank or NBFC, repaid in fixed EMIs over a defined tenure.

🔑 Key Features:

- Fixed interest rate

- Fixed EMI

- Fixed tenure (1–5 years)

- No collateral required

👍 Advantages of Personal Loans

- ✅ Lower interest than credit cards

- ✅ Structured repayment (EMIs)

- ✅ Suitable for large expenses

- ✅ Predictable financial planning

👎 Disadvantages of Personal Loans

- ❌ No interest-free period

- ❌ Processing fees

- ❌ Prepayment charges (sometimes)

⚖️ Credit Card vs Personal Loan: Detailed Comparison

| Feature | Credit Card | Personal Loan |

|---|---|---|

| Type | Revolving credit | Fixed loan |

| Interest Rate | 30%–45% | 10%–18% |

| Repayment | Flexible | Fixed EMIs |

| Best For | Short-term spending | Large expenses |

| Approval Time | Instant | Few hours to days |

| Rewards | Yes | No |

| Discipline Required | High | Medium |

🧠 When Should You Use a Credit Card?

Use a credit card if:

- 🛍️ You have small, short-term expenses

- 💸 You can repay within the interest-free period

- 🎁 You want rewards/cashback

- 🚨 You need emergency instant funds

👉 Example: Online shopping, utility bills, travel bookings

🧠 When Should You Choose a Personal Loan?

Choose a personal loan if:

- 💍 Wedding expenses

- 🏥 Medical emergency

- 🏠 Home renovation

- 🎓 Education or big purchases

👉 Ideal for large expenses that need structured repayment

💸 Cost Comparison Example

Let’s understand with a simple example:

Scenario: ₹1,00,000 borrowing

💳 Credit Card:

- Interest: ~36% annually

- If unpaid → ₹36,000 interest/year

💰 Personal Loan:

- Interest: ~12% annually

- Interest: ₹12,000/year

👉 Personal loan is 3x cheaper in this case

⚠️ Hidden Charges to Watch

Credit Card:

- Late payment fee

- Over-limit fee

- Cash withdrawal charges

Personal Loan:

- Processing fee (1%–3%)

- Prepayment penalty

- Late EMI charges

📊 Impact on Credit Score

Both affect your CIBIL score (managed by TransUnion CIBIL):

Credit Card:

- High usage → Negative impact

- On-time payment → Positive impact

Personal Loan:

- EMI discipline improves score

- Default damages score heavily

🚨 Risk Comparison

| Risk Factor | Credit Card | Personal Loan |

|---|---|---|

| Debt Trap | High | Medium |

| Overspending | High | Low |

| Default Risk | High interest burden | EMI pressure |

🧠 Expert Advice: Which Is Better?

👉 Choose Credit Card if:

- You are financially disciplined

- You repay full amount monthly

- You need short-term credit

👉 Choose Personal Loan if:

- You need large funds

- You want lower interest

- You prefer structured repayment

🎯 Final Verdict

There is no “one-size-fits-all” answer:

- 💳 Credit Card = Best for short-term, small expenses

- 💰 Personal Loan = Best for long-term, large expenses

👉 If used wisely, both can be powerful financial tools.

👉 If misused, both can lead to serious debt problems.

📌 Pro Tips to Save Money

- ✔️ Always pay full credit card bill (avoid interest)

- ✔️ Compare loan offers before applying

- ✔️ Maintain low credit utilization (<30%)

- ✔️ Avoid unnecessary borrowing

✍️ Conclusion

Understanding the difference between credit cards and personal loans is essential for smart financial planning. While credit cards offer flexibility and rewards, personal loans provide stability and lower costs.

👉 The smartest strategy is to:

- Use credit cards for convenience

- Use personal loans for necessity

Money is not just about earning—it’s about managing it wisely. The right borrowing choice today can save you thousands tomorrow.