How to Improve CIBIL Score Using Credit Card – Complete Guide (India)

Your CIBIL score is one of the most important financial indicators in India. Whether you’re applying for a personal loan, home loan, or credit card, lenders rely heavily on your score to decide your eligibility, interest rate, and credit limit.

A credit card, if used wisely, is one of the most powerful tools to build and improve your CIBIL score quickly.

In this complete 2500-word guide, you’ll learn practical, expert-level strategies to improve your CIBIL score using a credit card.

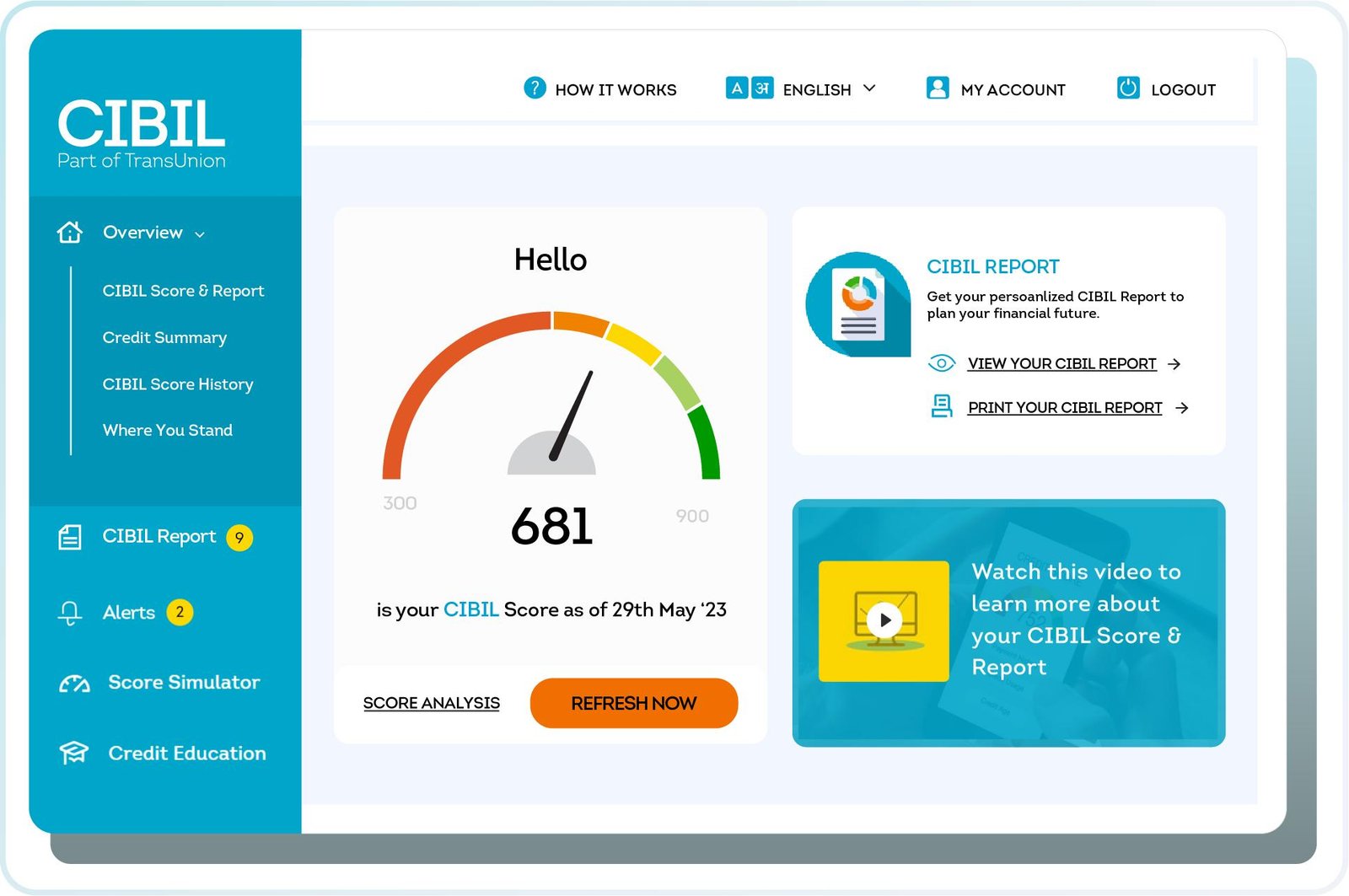

📊 What is a CIBIL Score?

A CIBIL score is a 3-digit number ranging from 300 to 900, issued by TransUnion CIBIL.

Score Range Meaning:

- 750 – 900 → Excellent (Easy loan approval)

- 700 – 749 → Good

- 650 – 699 → Average

- Below 650 → Poor (High rejection chances)

👉 The higher your score, the better your financial credibility.

💳 How Credit Cards Impact Your CIBIL Score

Credit cards influence your score through multiple factors:

1. Payment History (35%)

Timely payment of credit card bills has the highest impact.

2. Credit Utilization Ratio (30%)

How much credit you use vs your limit.

3. Credit Age (15%)

Older credit cards improve your score.

4. Credit Mix (10%)

Combination of secured + unsecured credit.

5. Credit Inquiries (10%)

Too many applications reduce score.

🧠 Why Credit Cards Are the Best Tool to Improve Score

Unlike loans, credit cards:

- Offer flexible repayment

- Allow monthly improvement tracking

- Help build long-term credit history

- Provide instant feedback on behavior

✅ 15 Proven Ways to Improve CIBIL Score Using Credit Card

1. Always Pay Bills on Time

Late payments can drop your score by 50–100 points.

Tips:

- Set auto-debit (NACH)

- Use reminders via apps like Google Pay or Paytm

- Always pay before due date, not last day

2. Maintain Low Credit Utilization (Under 30%)

If your limit is ₹1,00,000 → keep usage below ₹30,000.

Why?

High utilization signals credit dependency, reducing score.

3. Pay Full Amount (Avoid Minimum Due Trap)

Paying minimum due:

- Adds high interest (30–42% annually)

- Hurts credit score over time

👉 Always pay Total Outstanding Amount

4. Increase Your Credit Limit

Higher limit = lower utilization ratio

Example:

- Limit ₹50,000 → spend ₹20,000 → 40% utilization ❌

- Limit ₹1,00,000 → spend ₹20,000 → 20% utilization ✅

5. Keep Old Credit Cards Active

Old cards increase:

- Credit age

- Trustworthiness

👉 Use them occasionally for small payments.

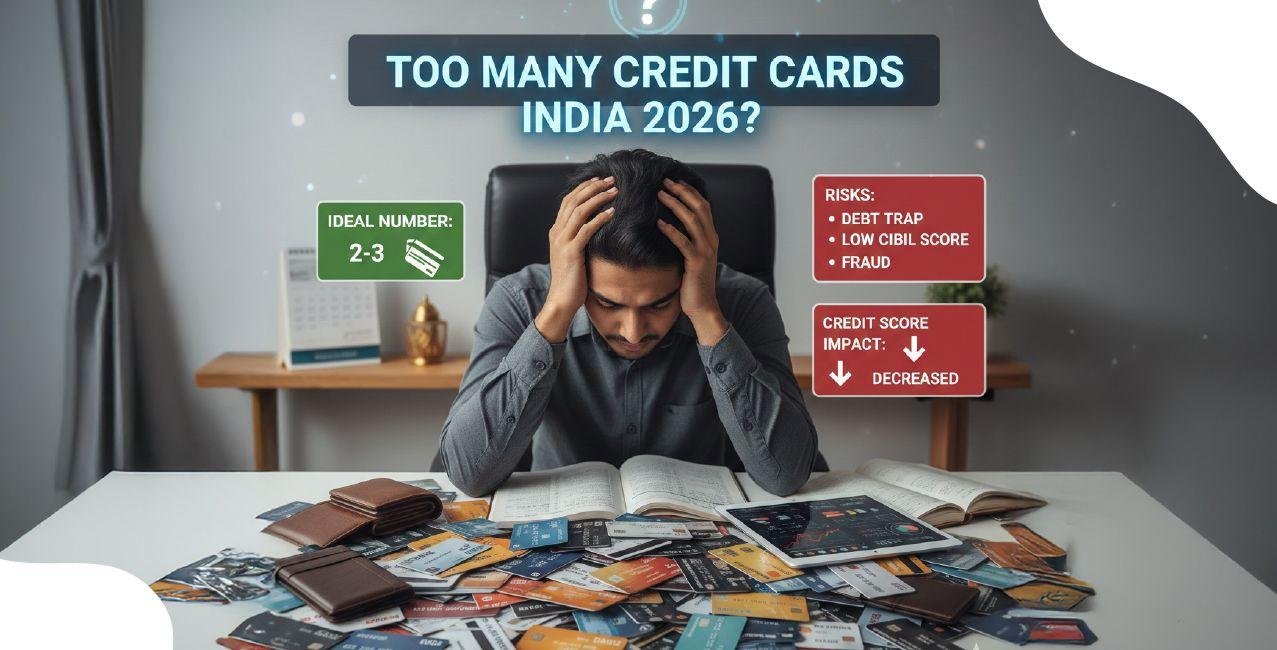

6. Avoid Frequent Credit Card Applications

Each application creates a hard inquiry.

Impact:

- Too many applications → negative signal to lenders

👉 Apply only when needed.

7. Use Multiple Cards Smartly

Distribute spending across cards:

- Keeps utilization low

- Improves credit mix

8. Convert Large Purchases into EMI

Using EMI:

- Reduces immediate burden

- Ensures structured repayment

But:

👉 Don’t overuse EMI — too many active EMIs reduce score.

9. Monitor Your CIBIL Report Regularly

Check via:

- TransUnion CIBIL

- Experian India

Why?

- Detect errors

- Track improvements

- Avoid fraud

10. Correct Errors Immediately

Common errors:

- Wrong late payment

- Duplicate loans

- Closed accounts still active

👉 Raise dispute on CIBIL website.

11. Don’t Max Out Your Credit Card

Maxing out card = high-risk borrower signal

12. Maintain a Healthy Credit Mix

Combine:

- Credit cards (unsecured)

- Loans (secured)

👉 Shows balanced financial behavior.

13. Avoid Closing Credit Cards Frequently

Closing cards:

- Reduces credit age

- Lowers total limit

👉 Keep old cards open unless high annual fees.

14. Use Credit Card Regularly (But Smartly)

Inactive card = no improvement

Ideal usage:

- Grocery

- Fuel

- Utility bills

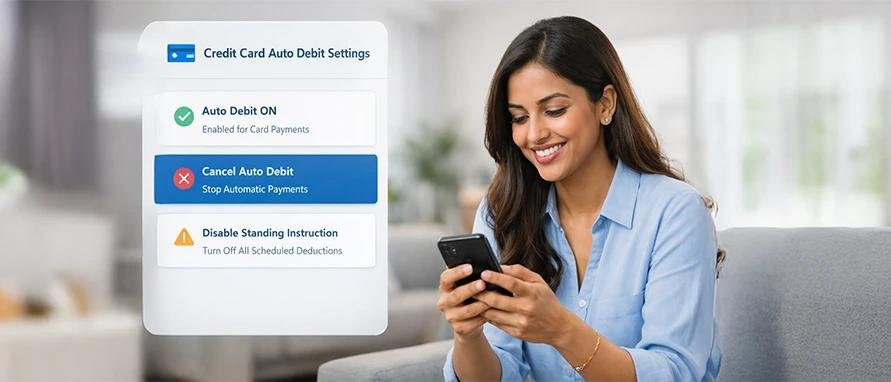

15. Set Auto-Pay for Safety

Auto-pay ensures:

- No missed payments

- Consistent score improvement

⏳ How Long Does It Take to Improve CIBIL Score?

| Action | Time Impact |

|---|---|

| Timely payments | 1–3 months |

| Reduce utilization | 2–4 months |

| Fix errors | 30–45 days |

| Build history | 6–12 months |

👉 Consistency is key.

🚫 Common Mistakes to Avoid

- Paying only minimum due

- Missing due dates

- Applying for too many cards

- Maxing out credit limit

- Ignoring credit report errors

📈 Pro Strategy (Expert Level)

If you want fast improvement (within 3–6 months):

- Use only 20–30% limit

- Pay 100% bill before due date

- Keep oldest card active

- Avoid new credit applications

- Track score monthly

🏆 Real Example

Case: Rahul (Delhi)

- Score: 620 → 780 in 6 months

What he did:

- Paid all dues on time

- Reduced utilization from 80% → 25%

- Stopped applying for new cards

- Used one card consistently

👉 Result: Eligible for home loan at lower interest rate

Improving your CIBIL score using a credit card is not complicated—but it requires discipline.

Golden Rules:

- Pay on time

- Keep usage low

- Avoid unnecessary credit

- Monitor regularly

A credit card can either destroy your credit score or make it excellent—the choice depends on how you use it.

🎯 Final Tip

Treat your credit card like a debit card with benefits, not free money.